2 min

2 min

Double income: If you have a loan for two, higher loan amounts may be possible. The requirement is the submission of both salary documents.

From a loan amount of CHF 80,000, the contract can be entered into with both spouses or both partners as contracting parties and thus as joint debtors.

This offer is primarily intended for registered partnerships and marriages. Partnerships that are not registered, or cohabiting couples cannot conclude a loan for two.

In the event of separation, divorce, or dissolution of the marriage or registered partnership, each contracting party is still liable and the financial responsibility of the joint debtors remains unchanged.

Social and economic changes require new, flexible financing options. Whether it's financing your home or implementing other projects, a loan for two offers you as a couple an additional degree of financial freedom and security.

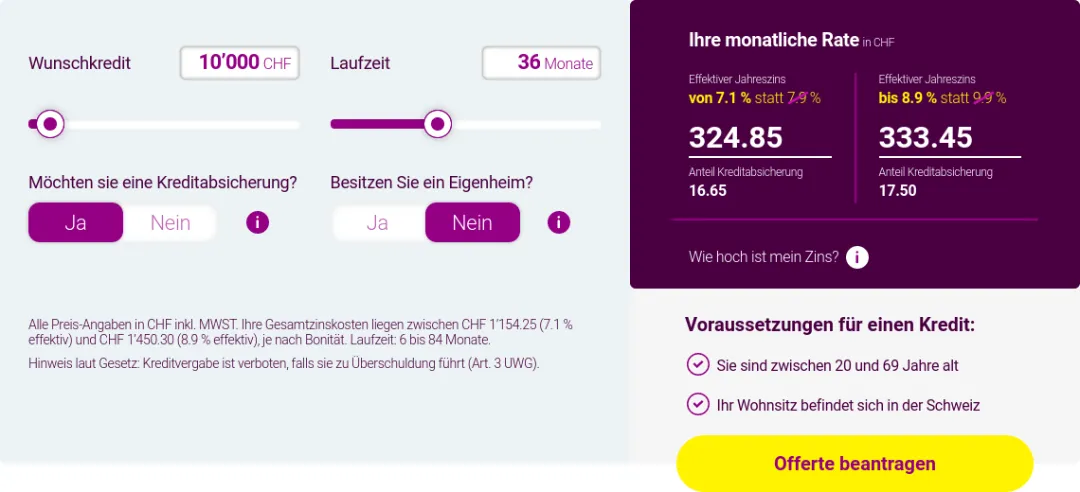

In a partnership, both parties often contribute to household income. BANK-now recognizes this added value and therefore enables you to conclude a loan agreement together. The requirement is the submission of salary documents for both spouses or registered partners. Sharing the cost of living increases your financial flexibility, which in turn opens up access to higher loan amounts. This can be particularly beneficial if you are planning major investments that your individual income alone could not cover.

From a certain loan amount, both partners can be listed as joint debtors in the loan agreement. According to the Swiss Consumer Credit Act (KKG) , this limit amount is from CHF 80,000. This option provides a clear definition of responsibilities. In the event of separation, divorce, or dissolution, both contracting parties must continue to meet the financial obligations.

BANK-now's loan offer for joint loan applications is tailored specifically to the needs of registered partnerships and married couples. Other partnerships that are not registered are excluded. A special advantage of this loan offer is the possibility of submitting joint applications. By submitting the documents from both partners, potential questions or ambiguities can be resolved in advance. The higher budget creates more leeway and can lead to a higher loan amount.

Ein Kredit zu zweit ist weit mehr als eine rein finanzielle Transaktion. Er ist ein Ausdruck von Vertrauen und gemeinsamen Zielen, die Sie als Paar verfolgen. Mit den massgeschneiderten Lösungen von BANK-now haben Sie die Möglichkeit, Ihre finanzielle Zukunft auf eine solide Grundlage zu stellen. Nutzen Sie die Gelegenheit und lassen Sie sich beraten, um das Potenzial eines gemeinsamen Kredits voll auszuschöpfen.